The original post is by our Vivek Bothra and the original post appears here.

In Jan’ 2015, almost a year back, diversified firm Max India spin-off plan were announced management indicated it is splitting listed entity into three companies with the existing firm becoming India’s first listed company with insurance as the sole business.

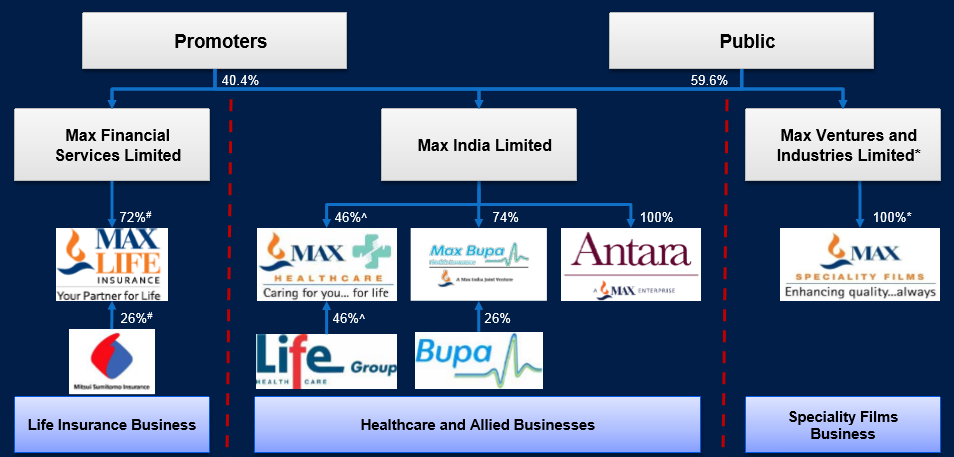

The Max India Group is a multi-business corporate, the listed entity has following primary business

- Life Insurance – As a 74: 26 Joint venture with Mitsui Sumitomo of Japan

- Max healthcare – Operating as equal JV with Life group of South Africa

- Health Insurance – As a 74: 26 Joint venture with BUPA of UK

- Antara – 100% owned retirement living real estate venture

- Max speciality Films – 100% owned

Last year the conglomerate began a demerger exercise which will result in listed company being split into three listed companies as per below:

Source – Investor presentation, Nov 2015

In this brief post, we try to examine if the sum of parts would be greater or lesser than the current M-cap. Let’s go to the drawing board.

Max Financial services – The largest piece of the spun-off entity is a well-established life insurance provider in India. Life Insurance is a crowded place in India where on one hand we have behemoth LIC, while on the other hand, you have well-funded strong private players like ICICI Prudential, HDFC Life and SBI. Apart from these, there are more than dozen challengers all gunning for the growing middle-class population in the country where life insurance coverage is abysmally low even compared to developing countries. It’s a highly competitive market with lot of pricing pressure on incumbents especially from new challengers. However, the size of the pie will ensure all players will have decent opportunity to grow.

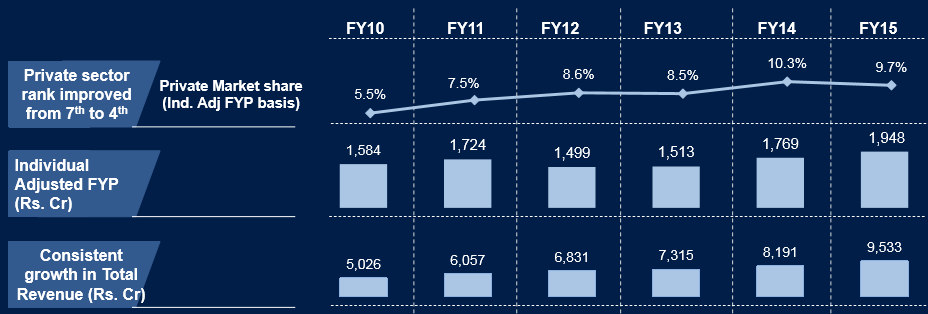

Max Life insurance is currently 4th largest private life insurer, it claims to have Industry best margins and RoEV an industry term which expands to Return on Embedded Value (in life insurance). RoEV shows the after-tax profit as a percentage of the equity on an embedded value basis (ie valuing all existing contracts at present day values).

Insurance is a very difficult business to value and Buffett also touches on what makes valuing an insurance company difficult. An investor has to trust that the firm’s actuaries are making sound and reasonable assumptions that balance the premiums they take in with the future claims they will have to pay out as insurance payments. Few errors can ruin a firm, and risks can run many years out, or decades in the case of life insurance.

However we have some pointers,

- A) In August 2012 the life insurance piece was valued at INR 10,500 Crore

Japan’s Mitsui Sumitomo Insurance Co. Ltd said it will purchase a 26% stake in Max New York Life Insurance Co., a joint venture between Max India Ltd and US-based New York Life Insurance Co., for Rs. 2,731 crore in an all-cash transaction.

The transaction values Max New York Life at more than Rs. 10,500 crore and is the second largest foreign direct investment (FDI) in the Indian life insurance industry.

Max Life bought Axis Bank’s 1% stake in the same year at INR 103.5 crore valuing the full business at INR 10,350 Crore with a put option to acquire remaining 3% stake in Oct’14 , 15 and 16.

However come 2015, There is change in heart

The details of this deal are not out but what made a partner take a reverse turn ? But overall this a positive move,

Also, post 2012, the business has gone from strength to strength increasing revenue by almost 40% from FY12 to FY15 and its competitive position improved.

If Mitsui Sumitomo’ s price paid follows the trajectory of revenue than this piece could be worth around ~INR 14700 Crores

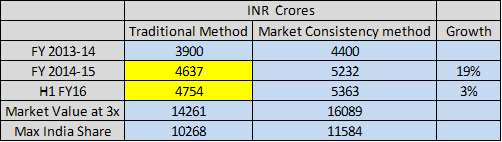

- B) There is another way to look at life insurance business, Insurance operations are often acquired at multiples of embedded value (EV) , Embedded value is the value of in-force business plus the value of the free capital. The management has indicated that recent deals in the insurance industry have happened at 3X EV.

As per November 2015 analyst presentation EV of life insurance, business is INR 5363 Crore and to complicate matters Max India has moved to market consistency method in last fiscal. The Market consistency method overstates EV. So we have to work with EV based on both methods.

In above tables items in yellow are estimated EV based on traditional method, therefore EV is INR ~ 4754 crores.

Based on above market value of life insurance business could be around ~INR 14,260 Crores using Traditional Method and ~INR 16089 using the market consistency method

With above two data points and make no mistake, I am no insurance industry expert so take everything I am writing with a pinch of salt.

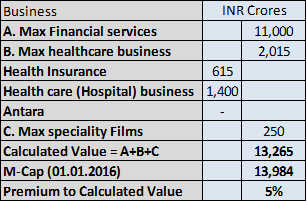

The value of Life insurance business would be between ~INR 14250 crore to ~ INR 16000 crore. Max India’s share with 72% ownership would be around ~INR 11000 Crore

Max healthcare business – This is the second largest piece of this spin-off, This entity will have three business under its umbrella

Health Insurance – In 74:26 JV with Bupa, In November 2015, Bupa announced that it is paying INR 191 Crores for 23% stake in health insurance business, This announcement pegs the value of health insurance business at ~ INR 830 Crore. With a 74% share, Max India’s current share would be ~INR 615 Crores

Health care (Hospital) business – This business is in recovery mode, They are very much North India focused business. Looking at FY16 profit and assigning a PE ratio would be inappropriate to put a value on this business. leading brokerage use EBITDA multiple. For H1 FY16 EBITDA was ~97 INR Crore, with a full year estimate of EBITDA of ~INR 200 Crore and using a multiple of 14, the value of health care business could be around ~INR 2800 Crore. At corporate level the company is almost debt-free so no debt is deducted for this calculation. Max India owns half of this business so their share would be ~ INR 1400 Crore

We have used 14x exercising some conservatism

ICICI Direct has used 16x for Apollo in August 2015, However Apollo is market leader with better ROCE than Max India

Antara – A 100% owned retirement living real estate venture. This business is in development mode the management has commented below in FY15 annual report

Senior Living as a business represents a tremendous opportunity in a nascent market and Antara Senior Living is extremely well positioned to execute the Dehradun project successfully and review opportunities for building its next community in the NCR region.

FY 15 it lost 50% of its net worth, Although Management is optimistic about its future, I can’t a put a number to this component so we value this piece as ‘Nil’

So overall Max India’s Max Health care share could be roughly valued at ~INR 2000 Crore

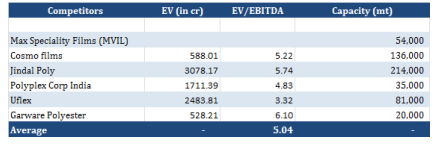

Max speciality Films – This will be the smallest spun off entity with FY16 estimated annual turnover of ~INR 800 Crore and EBITDA of ~INR 100 crore. Another blogger has done some great work on this piece of spin-off. The industry analysis is sourced from the blog

At average industry multiple, the value of this piece should be around ~INR 500 Crore. However, if we go by what promoters are saying this piece of business is valued at ~INR 168 Crore. In Jan’15 – this is what promoters have said,

The promoter of Max India, Analjit Singh, today announced his intention to make a voluntary open offer for buying upto an additional 34.5% stake in Max Ventures and Industries Limited (MVIL), which will be listed post the demerger of Max India, as announced earlier today, and which will hold the investment in Max Speciality Films Limited (MSF Ltd)…. listing of MVIL at an approximate valuation of Rs. 168 Cr. for 100% of MVIL.

On a conservative note, we will assign a value of ~INR 250 Crore for this piece of spin-off.

Putting the jigsaw together

At the current m-cap we are paying about 5% premium over our conservatively built total value of each unit. There is no free lunch on offer here but bear in mind most of businesses are growing and now they will get undivided dedicated management attention. Also, life insurance business is not directly listed in India so may see some traction with investors. In the past, these kind of spin-offs have resulted in value unlocking.

I will be delighted to get more inputs from you in comments

Disclosure – I am long with a tracking position to see how events unfold.

Caution – I have made many mistakes in past in analysing spin-off situations, don’t lose your salt by getting swayed by this post.